There are numerous factors at play in today’s natural gas marketplace that account for the strong market conditions. The current production levels, demand characteristics and transportation availability are all contributing to the sustained high natural gas prices throughout North America. This article will examine the production characteristics in the Western Canada Sedimentary Basin (WCSB). The supply trends over the 1990s provide us with an understanding of the development of this basin, and offer insight regarding future infrastructure and investment requirements which will allow this basin to continue to supply natural gas to the growing North American marketplace.

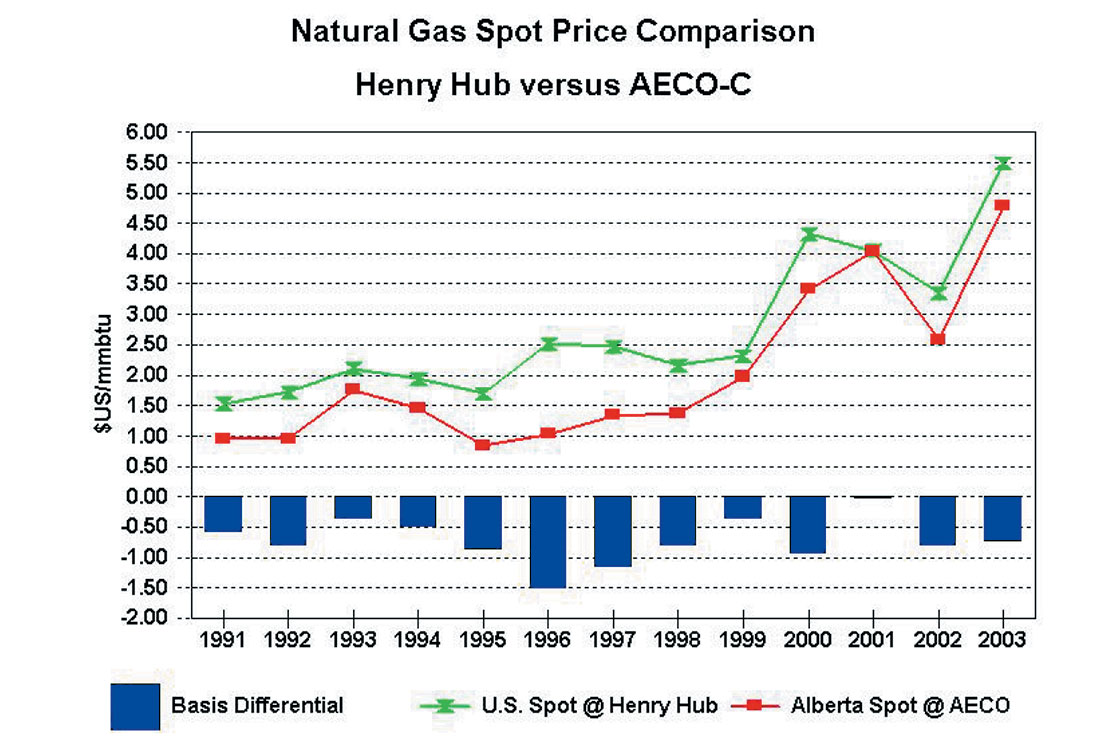

Not so many years ago, the market conditions for the Western Canada natural gas industry were quite different. Increasing production levels throughout the 1990s outstripped export pipeline capacity away from the region, creating a “gas bubble” within Western Canada. Gas-on-gas competition within the basin translated into lower netback prices for natural gas producers selling their natural gas into the local Alberta market. Natural gas prices in Alberta from Jan. 1990 to Dec. 1999 averaged $C 1.71/mmbtu. The difference between the Alberta price and the U.S. Gulf Coast price at Henry, Louisiana, called the basis differential, reached an all-time high in 1996, as illustrated on the next graph.

Frustration among producers unable to realize stronger netback prices through export sales created the incentive for the existing export pipeline system to expand, as well as initiated the development of the Alliance Pipeline Project. The Northern Border expansion, which occurred in late 1998, added about 700 MMCF/D of export pipeline capacity into the U.S. Midwest market region and the Alliance Pipeline, completed in late 2000, added about 1.5 BCF/D of new pipeline capacity into the same region.

Export pipeline capacity from the WCSB finally exceeded basin deliverability and natural gas prices in Alberta enjoyed a closer correlation to prices in markets throughout North America. Western Canada natural gas prices have benefited from the strong natural gas prices throughout North America this decade, with the Alberta natural gas price averaging $C 5.58/mmbtu from Jan 2000 to March 2004.

After the Alliance Pipeline was completed, annual supply growth was strong, and the big question back then was how soon this incremental pipeline capacity would fill up. Now, there seems little doubt that spare pipeline capacity out of the WCSB will continue, at least until significant new supply becomes available, either through northern frontier natural gas supply or significant growth in unconventional supply such as coalbed methane and tight gas. Despite record levels of natural gas drilling activity, deliverability is not increasing. Conventional supply, in this basin, is “on the treadmill”, with flat or even declining deliverability, as illustrated on the following graph.

This rate versus time plot using a coordinate scale illustrates historical production performance of natural gas wells in the WCSB. Wells have been grouped by on production date and the resulting production profiles clearly show the contribution of recent drilling to total production in this basin. Seasonality of production is also clearly defined, as are production decline rates. After many years of production growth out of the WCSB, production levels have flattened out. Strategies utilized by many producers including in-fill drilling and a focus on shallow, development type drilling has led to a situation of steep initial decline rates and low initial well rates for the record number of natural gas wells connected in this basin. Between 3 to 4 BCF/D of incremental production must come on each year to replace production lost to production declines. Decline rates per well grouping indicate the pre-1996 wells are declining at approximately 10 percent and flattening. The productivity profiles of recent well additions exhibit a very steep initial decline, such that, at present, a basin decline of approximately 25 percent is apparent with an expected flattening to a decline of around 20 percent.

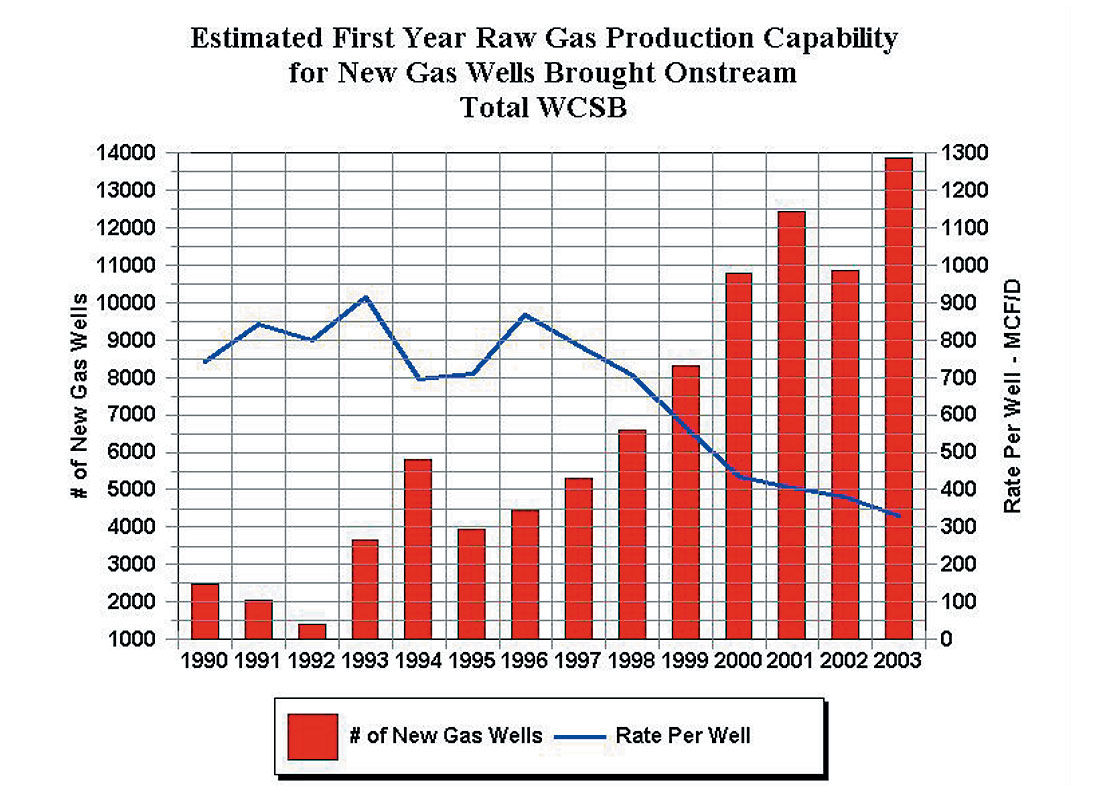

The above graph illustrates the average first year deliverability of wells placed on production in the WCSB. The number of new gas wells reflects wells that recorded production during the year. Average well rates have been steadily dropping since 1996, although the downward inclination appears to be moderating somewhat since 2000. Whether this trend continues will depend on the type of natural gas drilling in the WCSB. If the drilling focus continues to remain predominately on shallow gas wells, then we expect to see continued high drilling levels, steep initial decline rates and low initial well rates. A drilling trend toward better quality reserves, though, should result in higher well rates and therefore, fewer wells would be required to grow production.

Because just over 70 percent of recent total WCSB natural gas production is from Alberta, the initial well rates for wells producing in this province have a large impact on the overall WCSB production characteristics. The average first year deliverability of wells placed on stream has been steadily dropping, despite the record number of natural gas well connections, due to the predominate focus on shallow gas well drilling. Initial rates vary regionally within the province, with wells producing in the southeast portion of the province registering very low initial rates while wells in the Foothills region produce at much higher rates. Because the vast majority of recent well connections have occurred in the southeast portion of Alberta, the provincial well rate is heavily influenced by the industry trend of drilling shallow, development type wells.

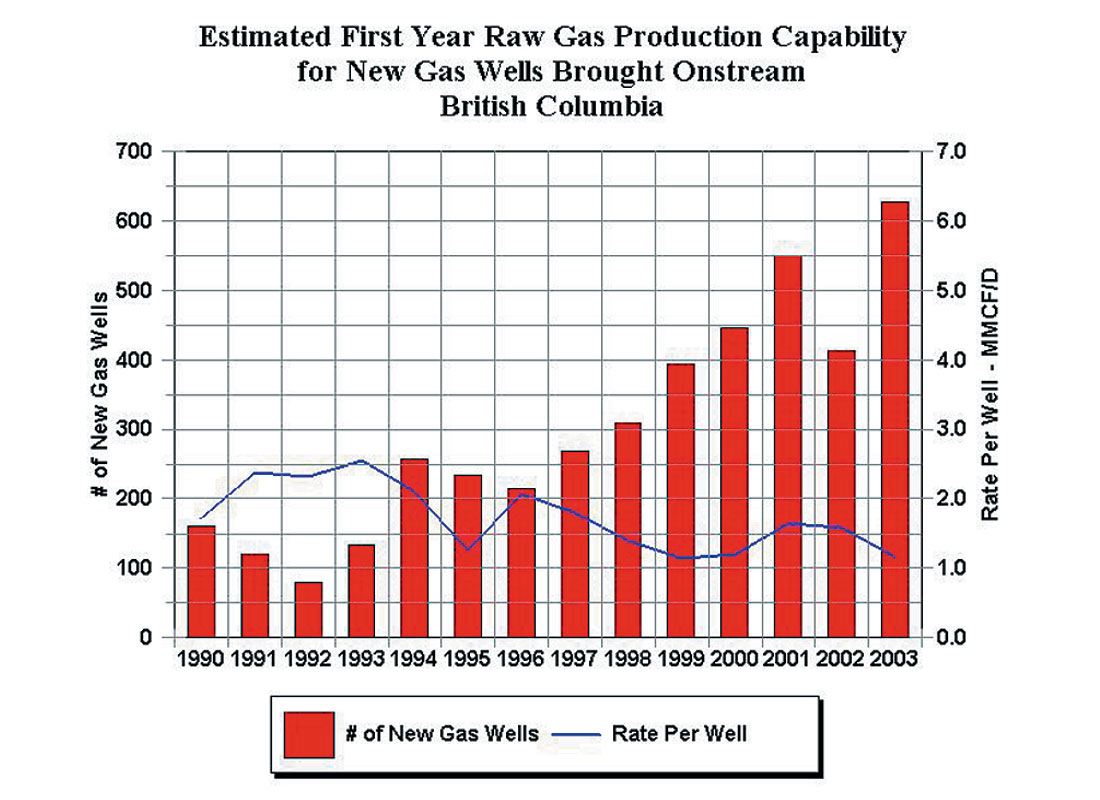

First year well rates for wells producing in British Columbia are much higher than the average well rate in Alberta, because the wells are generally much deeper and start producing at higher rates. However, initial wells rates are lower in 2003 relative to 2001 and 2002, at just above 1 MMCF/D.

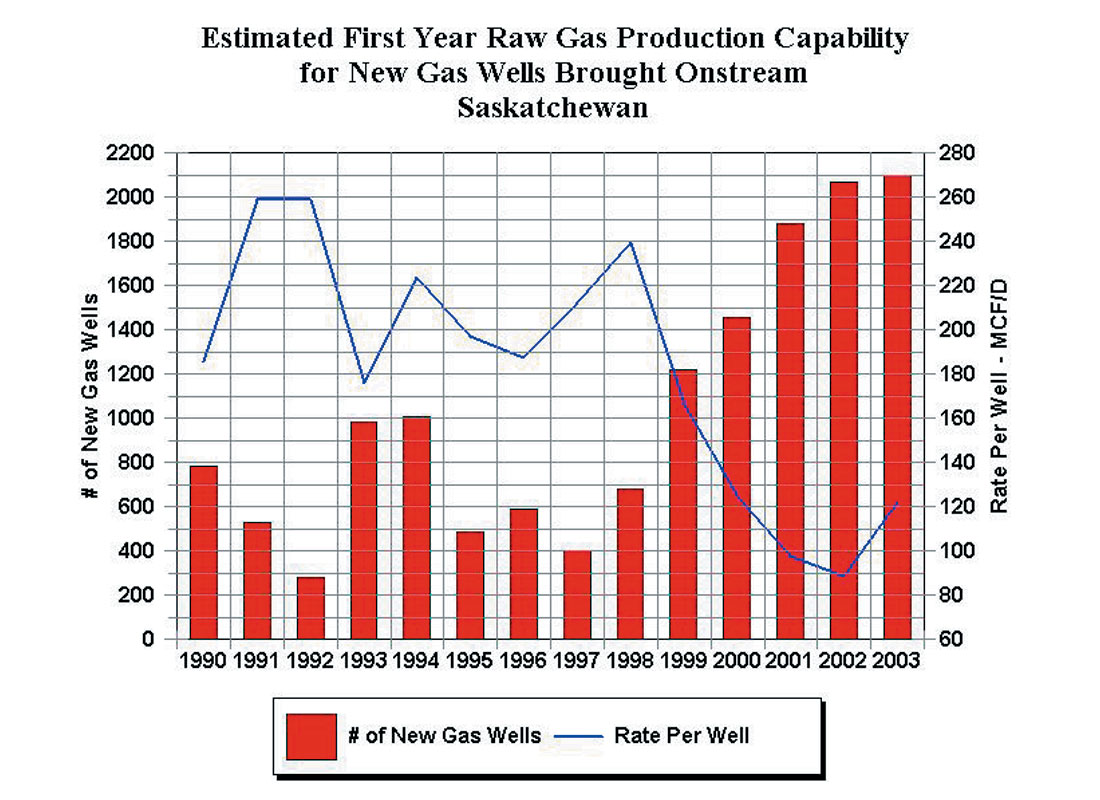

A surprising reversal of trend appears to have occurred in Saskatchewan since 2002, where initial well rates had been falling dramatically since 1998. Although initial well rates in the province are the lowest of the 3 provinces, the reversal in trend is surprising. Production is also up in this province between 2002 and 2003, a result of the higher quantity and quality of natural gas wells being drilled. Unfortunately, the overall contribution to natural gas production in the WCSB from Saskatchewan is a round 5%, so that an increase in initial rates from wells drilled in this province hasn’t had a significant impact on the overall basin initial well rates. That being said, it is very encouraging to see the reversal of trend in initial well rates.

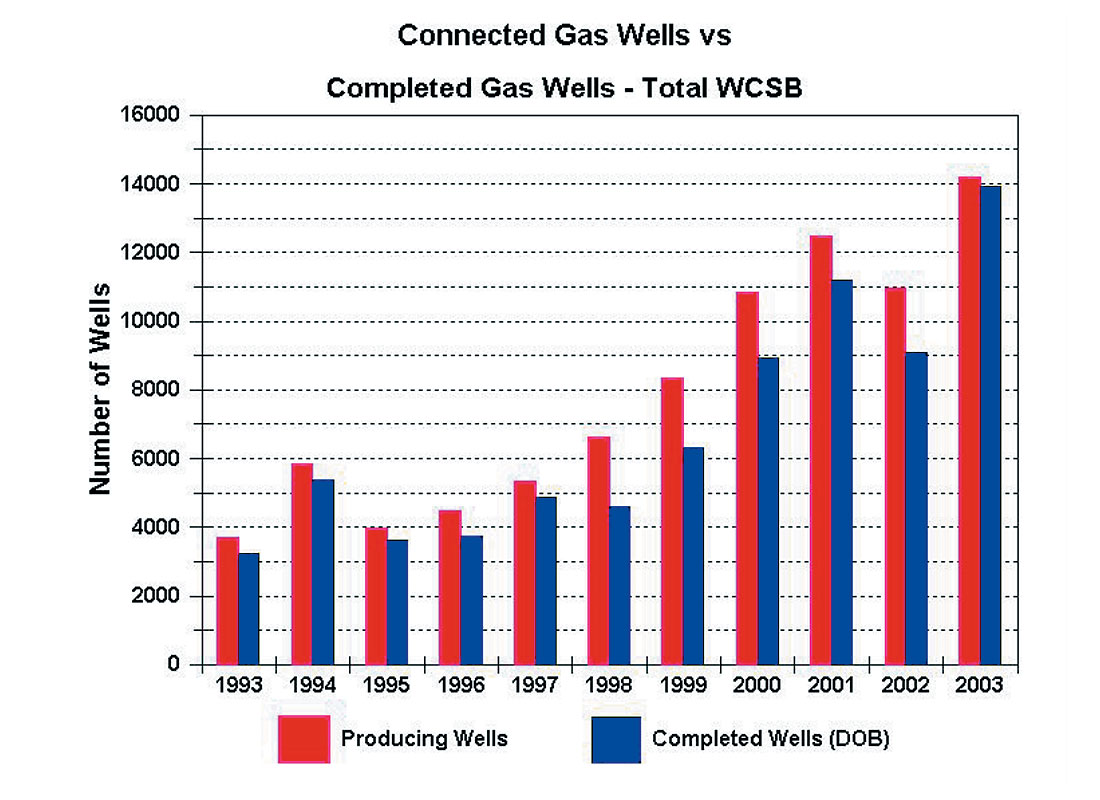

Another significant occurrence in the WCSB has been the production of unconnected reserves that took place from 1998 to 2002. During the regulated era (pre-1986) the natural gas industry had accumulated a large proved reserve base. After the natural gas industry was deregulated, low natural gas prices kept these unconnected reserves in the ground. The above graph highlights the difference between natural gas wells that recorded production throughout the year versus the number of reported completed natural gas wells during these years. Because there is usually a time lag between the completion and connection of a well, the two numbers are usually close, but not the same. In 1998, the natural gas industry in Western Canada was gearing up for the first significant export pipeline expansion to occur since 1993. Although natural gas prices were still quite low in 1998, the difference between the number of completed wells and the number of new producing wells indicates that large portions of previously unconnected reserves were connected. This trend continued in 2000 when natural gas prices improved dramatically, and combined with the completion of the Alliance Pipeline, marginal, previously uneconomic unconnected reserves were brought on production. In 2003, it appears that the historical relationship between completed and connected wells has returned . In the future, the industry will not have the "unconnected" portion of reserves available to bring on quickly as economic conditions dictate. Therefore, the natural gas industry has essentially move to "just-in-time" inventory management.

Despite the jump in overall natural gas drilling activity, the split between development drilling and exploratory drilling has remained fairly constant over the last 7 years, with a ratio of approximately 75% development wells, 25% exploratory wells, and the strengthening in prices apparently having little impact on the move north and west. Development drilling jumped by 58% between 2002 and 2003, while exploratory drilling jumped 41%.

From these production statistics, it is easy to see why the Western Canada natural gas industry is on a production “treadmill.” It is very important, though, to distinguish between the perception of running out of natural gas in this supply basin versus understanding the changing nature of the basin and determining how best to proceed with infrastructure and investment in order to continue to develop this resource to supply the North American marketplace. Natural gas resources in Western Canada remain plentiful, but no longer can inexpensively produced reserves continue to increase deliverability at rates seen in past decades. The future of natural gas deliverability from conventional production in Western Canada depends on the production characteristics of future natural gas wells. While the natural gas industry will continue to rely on inexpensive, shallow development gas well drilling, natural gas producers will also need to expand their efforts to more geographically remote and geologically complex exploratory drilling. The ability of the industry to do this will depend on an efficient regulatory process and successfully addressing environmental concerns. Infrastructure must also be available for processing and transporting the natural gas to mainline pipelines. Most importantly, natural gas prices must be sustained at a level to support the higher drilling costs and longer cycle time required to find and produce these deeper, higher quality reserves. The benefits of the current robust natural gas prices are expected to continue to accrue to Canadian producers, and reinvestment in exploration efforts will be necessary in order to get off the deliverability “treadmill” and achieve conventional production growth in the WCSB.

Join the Conversation

Interested in starting, or contributing to a conversation about an article or issue of the RECORDER? Join our CSEG LinkedIn Group.

Share This Article